Ahead of the UPI Transaction Limit increase from INR 1L to 5L for hospitals & educational institutions and MPC’s decision to keep the repo rate in India at 6.50%, several banks have now increased their FD rates up to 8%. MPC or Monetary Policy Committee led by the RBI governor released a circular on December 8, 2023, addressing the upcoming financial year's GDP projections and inflation projects. Here’s all you need to know about it and a list of banks' FD rates in December 2023 that have seen a rise.

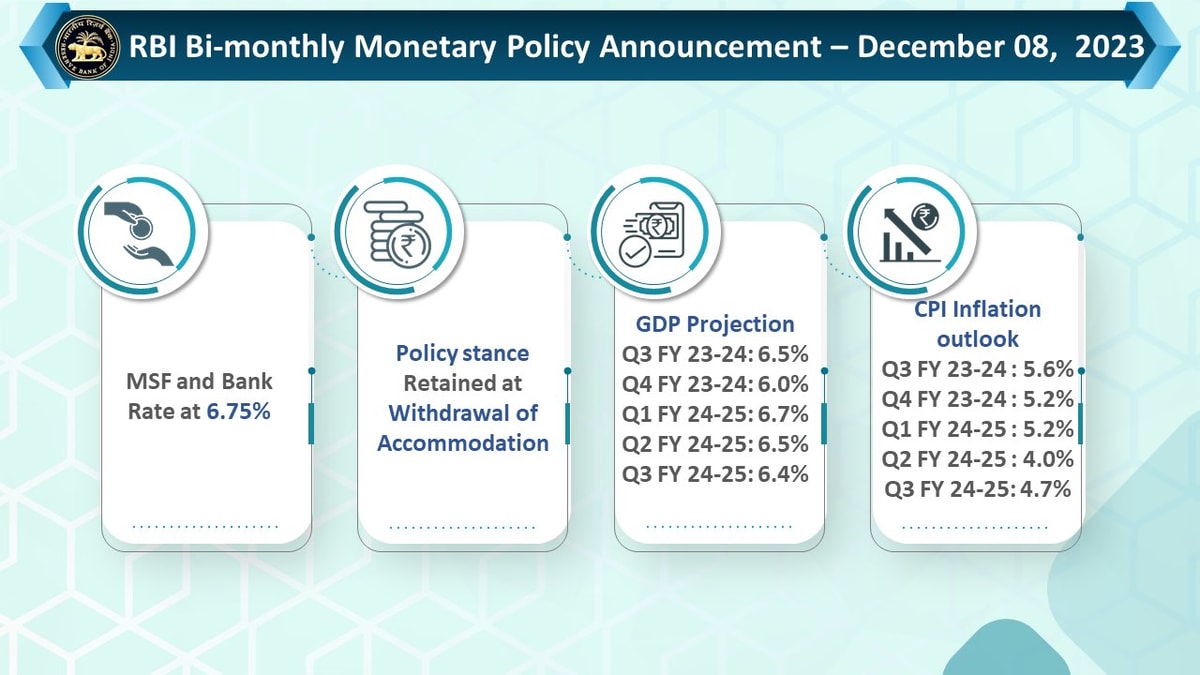

MPC Releases GDP & Inflation Projections for FY23 to FY24 (April 2023 - March 2024)

MPC or Monetary Policy Committee led by RBI in its key policy announcements on December 8, announced the GDP projects & inflation projections for the financial year 2023-2024. As per the official report, the GDP projection is 6.5% for Q3 FY23-24, 6.0% for Q4 FY23-24 and so on.

The World Bank data on the GPD growth in India from the year 1961 to the year 2020 displays a powerful historical rise of the Indian economy from 3.7% in the year 1961 to 9.1% in FY21-22.

A rise in the GDP generally signifies a growth in the country’s economy which means more opportunities for jobs, development and progress.

Recently, RBI also revised the UPI transaction limit from INR 1 Lakh to 5 Lakh for hospitals and educational institutions. Additionally, “RBI has proposed to enhance the additional factor of authentication (AFA) limit to ₹1 lakh per transaction (15,000 at present) for recurring payments of mutual fund subscriptions, insurance premium subscriptions and credit card repayments, to further accelerate the usage of e-mandates” read the circular.

While we are talking about mutual funds, insurance and credit cards, be sure to check out our Banking Offers & Deals group to know what are the latest saving offers you can avail.

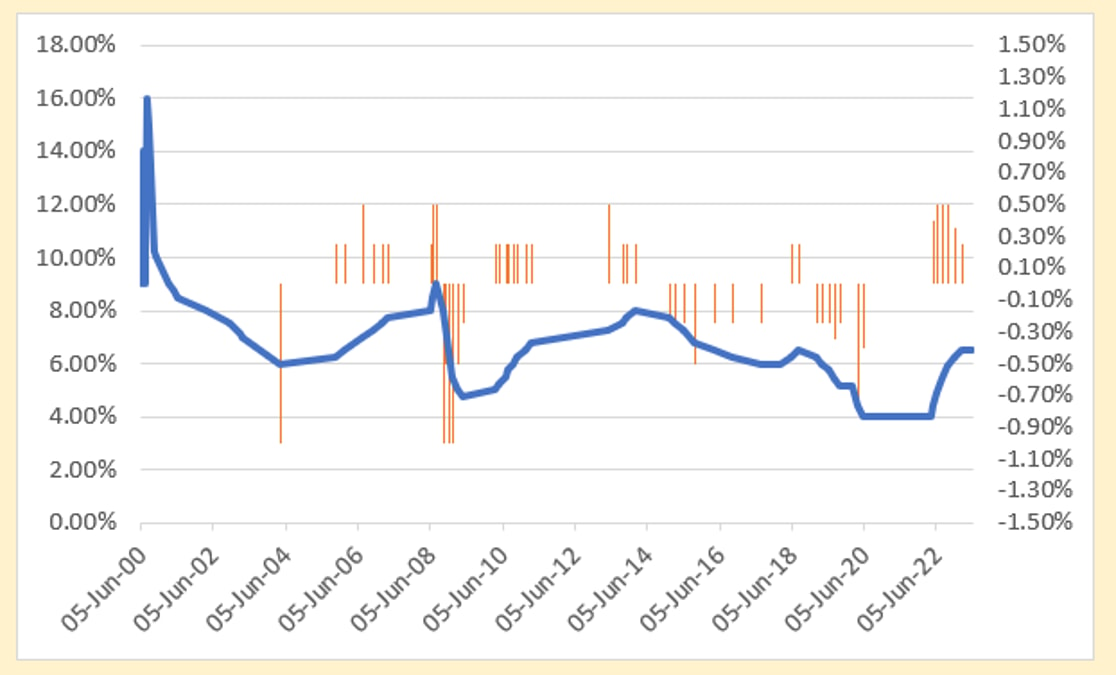

Repo Rate to Remain Unchanged at 6.50% for FY23 - FY24

In the same meeting held, RBI also emphasised their target to keep the repo rate unchanged at 6.5% for FY23 - FY24.

The RBI Governor highlighted that easing inflation across all components of retail inflation is one of the reasons behind the MPC's decision to keep the repo rate unchanged.

The above is historical data on repo rate in India

What does an unchanged repo rate mean?

An unchanged repo rate basically means that the rate at which the central bank lends money to commercial banks will remain unchanged. This leads to a more stable monetary stance between the bank & the central bank. Hence providing borrowers more security that their monthly EMIs will not increase.

Banks Increase FD Rates in December 2023

After the announcement of RBI keeping the repo rates unchanged at 6.50%, several banks have revised their current FD rates. This includes ICICI Bank, Kotal Mahindra Bank, HDFC Bank, Axis Bank, UCO Bank & more.

If you haven’t yet begun your mutual fund's investing journey, you could easily start it through stocks & investing apps such as Zerodha, Upstox, Groww, 5Paisa

While some banks like Axis has revised their FD rates on deposits above 5 Crore, there are some banks like ICICI who has revised FD rates w.e.f from December 14, 2023, for deposits above 2Cr. Kotak Mahindra FD Rates have also been revised and are increased by 85 basis points for fixed deposits below 2Cr. Below is list of the latest bank FD rates in December 2023.

Following, we have added the list of the updated FD rates of several banks such as ICICI Bank, Federal Bank, HDFC Bank, Axis Bank, etc.

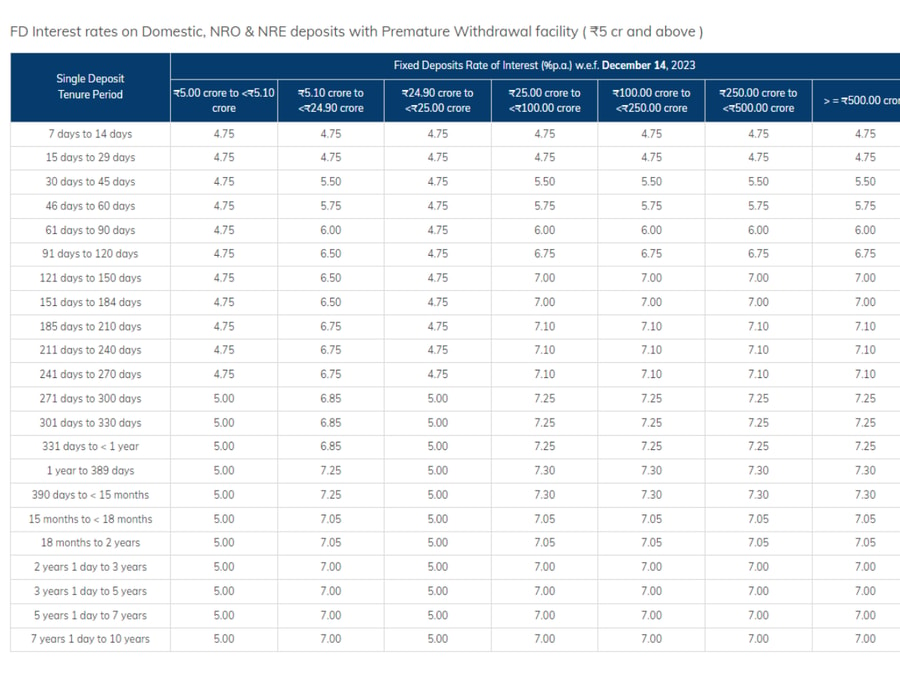

Here’s a list of the updated ICICI Bank FD Rates w.e.f from 14th December 2023.

ICICI Bank FD Rate (Effective from 14th December 2023)

ICICI Bank revised FD rates applying to deposits from Rs.2 Crores to Rs.100 Crores+. The FD rate for Rs.2 Crore FD in ICICI Bank now offers a 7.25% interest rate for 365 days and 7% for 180 days. Following are the FD rates ICICI Bank is offering now:

ICICI Bank Fixed Deposits Interest Rates for Domestic/ NRO / NRE effective from 14th December 2023

Single deposit of ₹2 Crores & above but less than ₹5 Crores

HDFC Bank FD rates are revised for FDs exceeding Rs 100 crore to Rs 500 crore. Earlier the interest was 7.35% which now stands at 7.30%. Below are the latest HDFC Bank FD Rates:

HDFC Bank FD Rates - Domestic/NRE/NRO Term Deposits for amounts equal & more than Rs. 5 Cr (Withdrawable)

HDFC Bank also recently crossed its 2.75 Lakh Crore mark in UP. The bank was also offering its HDFC Tata Neu Credit Card for lifetime free until 3 months back

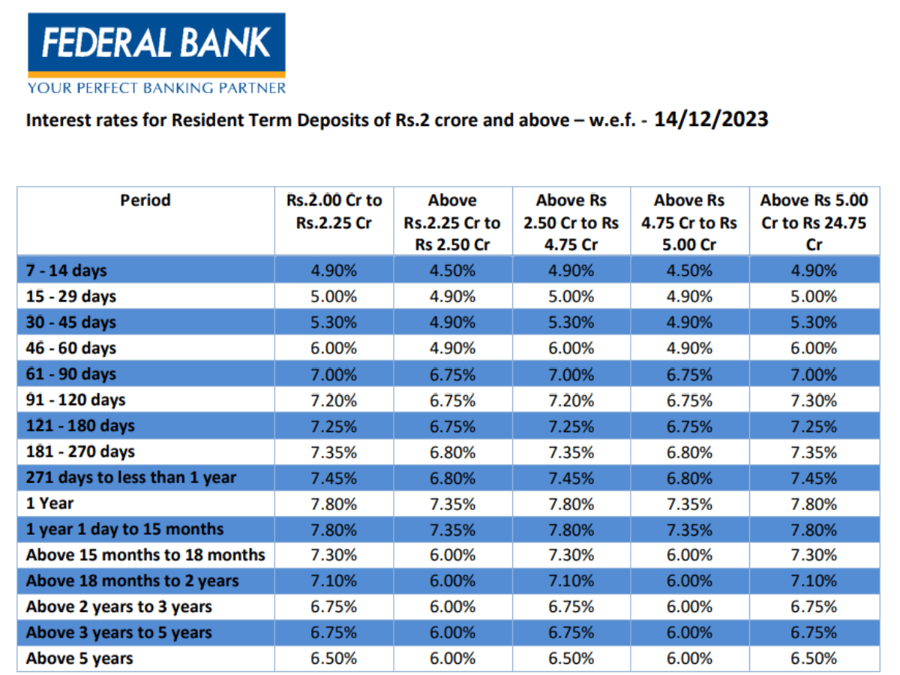

Federal Bank also revised its FD Rates on 14th December 2023 and is now offering 7.80% interest rate for 1 Year term deposit as opposed to 7.45% interest previously on Rs.2 Cr and above funds. The interest rate for 61-90 days period for 2 Cr to 2.25 Cr funds is now also increased to 7% from 6.50% interest previously.

Kotak Mahindra Bank FD Rates are revised for both regular and senior citizens w.e.f 11 December 2023. The highest interest rate customers can grab is 7.80 % for senior citizens for 23 months which was 7.75% previously. For regular citizens, the starting interest rate is revised to 3% from 2.75% previously for a period of 7-14 days. Below are the latest FD rates offered by Kotak Mahindra Bank:

Interest rates for Domestic/NRO/NRE fixed deposits effective from 11th December 2023

Bank of Baroda is considered as one of the good banks for high FD rates on deposits. Following are the latest Bank of Baroda Term Deposit interest rates:

₹2.00 Crores up to ₹5.00 Crores (w.e.f 14 December 2023)

Axis Bank Fixed Deposit Interest Ratesw.e.f 14 December 2023

Axis Bank fixed deposit interest rates are also revised on 14 December for funds ranging from 2Cr to 500 Cr and above. The bank has also been recently offering zero charges on issuing loan sanctions. Customers planning for a fixed deposit of 2 Cr and above can consider the following latest Axis bank FD rates:

So, this was all about sharing the latest Bank FD rates. After the announcement of the RBI governor’s decision to keep the repo rate unchanged at 6.50% for FY23-FY24, several banks as mentioned above increased their FD rates. There are also other banks such as DCB Bank, UCO Bank, Bank of India who have revised their FD interest rates for December month. We hope this article helps you plan your investment.

Vrushali is a content & copywriter with 3+ years of exp in writing, researching & ideating content pieces. She writes articles across finance, tech, lifestyle, telecom, online shopping & travel. When not working, you'd find her scribbling designs.

@some1anywhere All Bnaks and NBFCs are regulated by RBI. DICGC insurance is anyway till 5 lakhs and post talks about 2 crore plus. Anyway, my take on the same,

FD beyond 2 crores are for Corporate or HNI. Sr Citizens, yes, can have FDs, but since these FDs can not be prematurely broken, it does not make sense for them to invest here as they might require money anytime and with less hassle. Around 5 to 10% of Sr Citizen's corpus can also be invested in MF to beat inflation, and if they have surplus, even more can be done. Having medical insurance helps them to reduce expenses. For others, it is better to invest in a diversified portfolio like MF, stocks, real estate (may be as it is usually illiquid), bonds, small saving schemes, and FD.

For a salaried person, I like RD over FD as I can invest monthly like SIP.

PS I am not a registered investment advisor, though by education, I have full qualifications to do so. Have an interest in personal finance and manage my own finances.

@some1anywhere All Bnaks and NBFCs are regulated by RBI. DICGC insurance is anyway till 5 lakhs and post talks about 2 crore plus. Anyway, my take on the same,

FD beyond 2 crores are for Corporate or HNI. Sr Citizens, yes, can have FDs, but since these FDs can not be prematurely broken, it does not make sense for them to invest here as they might require money anytime and with less hassle. Around 5 to 10% of Sr Citizen's corpus can also be invested in MF to beat inflation, and if they have surplus, even more can be done. Having medical insurance helps them to reduce expenses. For others, it is better to invest in a diversified portfolio like MF, stocks, real estate (may be as it is usually illiquid), bonds, small saving schemes, and FD.

For a salaried person, I like RD over FD as I can invest monthly like SIP.

PS I am not a registered investment advisor, though by education, I have full qualifications to do so. Have an interest in personal finance and manage my own finances.

Good info there @arorasid but there's just one point I doubt here. I do not think all banks are regulated by RBI. Only scheduled banks are regulated by RBI, isn't it?

Keeping Rs 2 crore + in fd for mere interest can be workable only to senior citizens , retired people , else its foolishness for the other lot to keep such amount in bank fds rather than exploring other avenues or doing business

Makes sense to me..but I think if I am going to be keeping 2 Cr+ in FD, then perhaps more of my focus would be on parking my money in a safe investment than merely making the most buck out of it.. since that gives me decent returns yearly + perhaps can help tackle inflation..but then there would also be huge taxes of course.. please share if you have any more views on this Loaferg

Follow Us

Follow Us

VU for efforts. Install Stable Money or Moneycontrol. They have higher FD return bank options

Good info there @arorasid but there's just one point I doubt here. I do not think all banks are regulated by RBI. Only scheduled banks are regulated by RBI, isn't it?

The list of all the regulated/non-regulated banks in India can be found on this official RBI page - https://rbi.org.in/commonman/English/Scripts/Ba...